As Uganda accelerates its cashless ambitions, there is debate about whether it can truly leave cash behind

Kampala, Uganda | IAN KATUSIIME | Uganda’s financial ecosystem has made a tremendous shift towards mobile money transactions — led by platforms like MTN Uganda and Airtel Uganda — which now move trillions of shillings annually, turning even the smallest roadside kiosk into a node in a vast digital payments grid.

Agent banking has followed suit, with commercial banks extending their reach deep into trading centres and rural markets, collapsing the distance between formal finance and the informal economy.

Yet cash remains stubbornly dominant. In supermarkets, restaurants and for last-mile deliveries, a significant number of customers still reach for physical notes wary of network downtimes and transaction charges or simply out of habit.

For many small businesses, cash offers immediacy and simplicity: no settlement delays, no failed transfers, no digital trail. Even in urban centres where payment terminals sit on countertops, they often serve as a backup rather than the default.

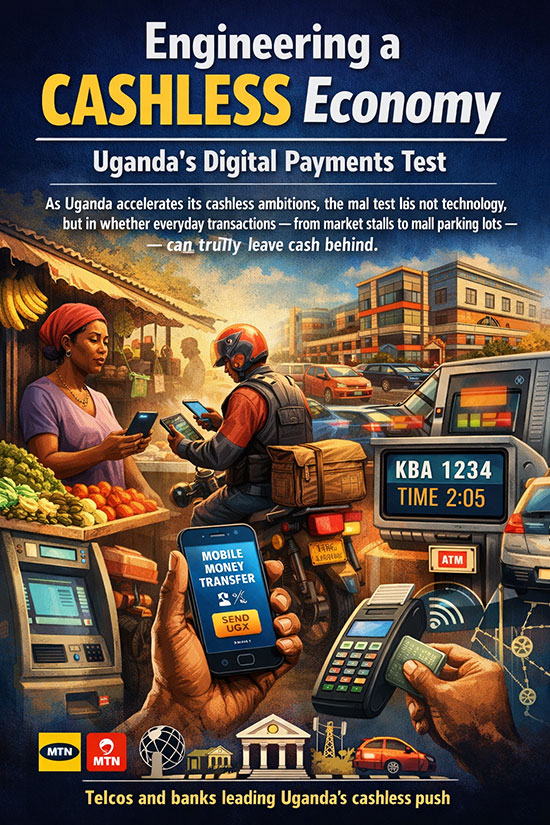

In other words, Uganda’s cashless ambition is not just a technological transition but a behavioral one. A simple example is the parking payments at two popular establishments: Acacia Mall and Lugogo Shopping Centre.

At Acacia Mall, parking is a seamless transaction where cameras read the number plate on entry, timestamp your stay, and bill the car owner. To pay, you enter the number plates into the payment platform, but payment is only in cash, leaving out the option of mobile money payments.

For Lugogo, motorists receive a ticket on entry which is either scanned or fed into a machine before you pay in cash. The digital payment option is left out. The barriers lift automatically, but questions have remained on what it would take to make the entire exercise a paperless and cashless endeavor.

This was the vision behind Uganda’s National e-payment Strategy 2021-2026. The strategy aims to foster a safe, efficient, and inclusive digital ecosystem, significantly reducing reliance on cash by enhancing infrastructure and regulatory frameworks.

The strategic goals were digital infrastructure development, reducing transaction costs, promoting interoperability between banks and mobile money, and enhancing consumer protection.

To achieve this, the government of Uganda enacted the National Payment Systems Act 2020 as a regulatory framework for payment systems, mobile money and electronic money issuers with oversight by the Bank of Uganda. The law is what would govern cryptocurrencies, although the latter remains a grey area in Uganda.

But the journey to making Uganda a cashless economy remains an uphill task because of factors such as corruption and a highly informal economy.

“Corruption could be the first issue,” says an expert in the fintech sector. “Cashless infrastructure is expensive to implement because the cost of transactions is high,” he added.

The expert said that Kenya and Rwanda built cashless economies because they were deliberate about it. In the two countries, virtually all services accept cashless payments, from high-end shopping to boda bodas and hawkers. Some services in Kenya and Rwanda can only be procured via digital payments, which remain elusive in Uganda.

In Uganda, services like boda boda and vendors are restricted to cash payments because of the convenience and a failure to grow a digital economy.

Some observers blame the rigid and predatory nature of the Uganda Revenue Authority (URA) that has led to tax evasion among service providers and those in the business community.

Lack of consumer protection

“We lack consumer protection in this country. Telcos and banks raise their fees without government objection,” a player in the financial sector told The Independent. “Here, if the board of MTN wants to meet a target, they just increase the tariff on a product.”

Telcos and banks are at the forefront of Uganda’s cashless push, building the digital rails from mobile wallets to agent banking networks to taps, scans and instant transfers. MTN introduced MoMo Advance, where customers can borrow mobile loans of up to Shs2m, which has promoted financial inclusion for Ugandans without the hustle and bustle of the paperwork that bank loans require. Airtel came through with QuickLoan.

But telcos still battle with the goal of a cashless economy. “Cash is the biggest competition because of its natural convenience,” says an industry source who prefers not to be named.

“Slow and minimal penetration of merchant payments in the rural and informal economy,” he says. The high perceived transaction costs, especially on withdrawals, have also permeated a culture where people prefer to keep their cash.